Economics

Economic Surplus: Definition & How To Calculate It

Here’s an overview of total surplus. Learn its definition, the different types of surplus, their uses, and how to calculate them

Sarah Thomas

Subject Matter Expert

Economics

03.31.2022 • 5 min read

Subject Matter Expert

The article explains the concept of economic resources with examples. It points out which are the different types and their relationship with scarcity, choice, and opportunity cost.

In This Article

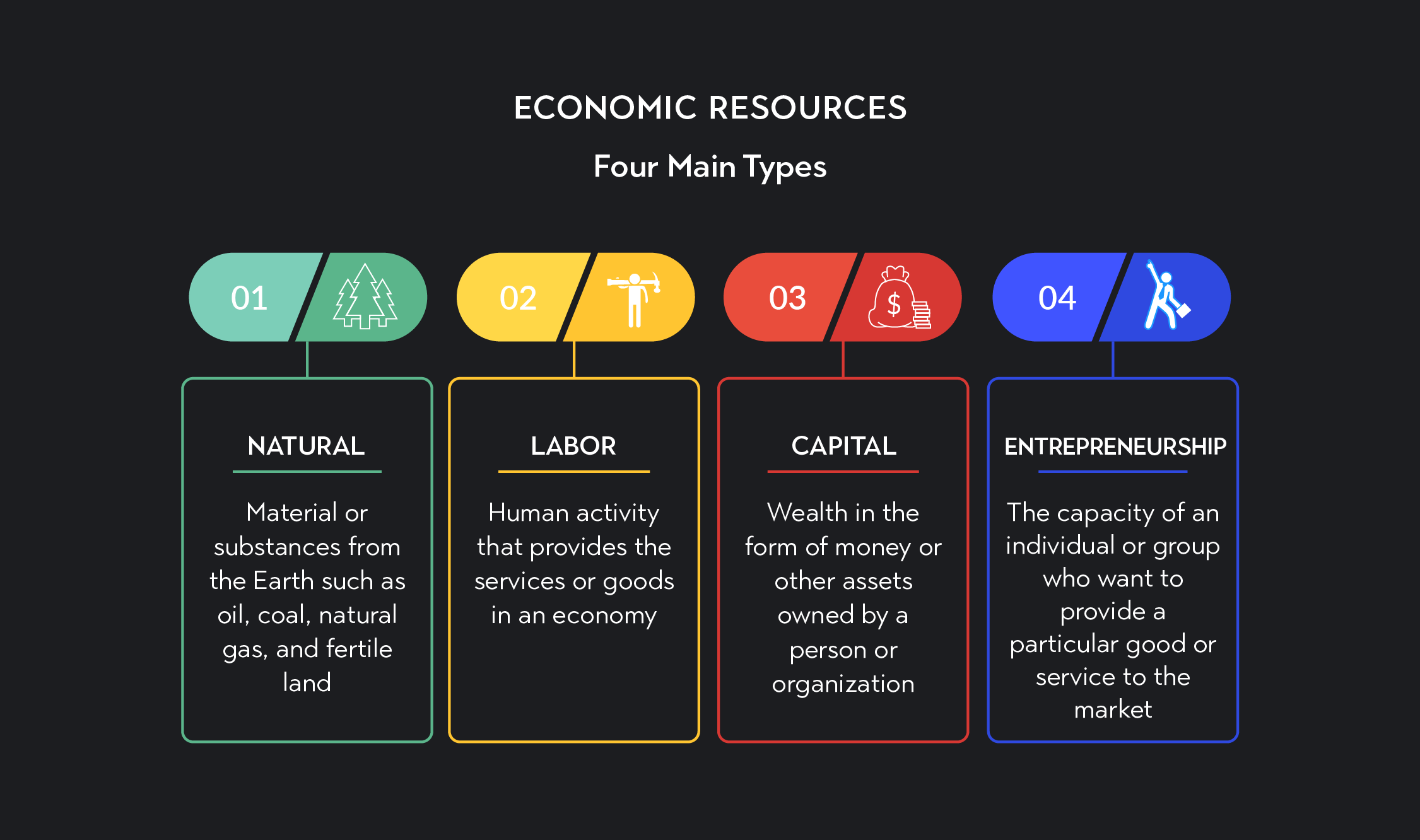

Economic resources are the different factors of production used to produce all goods and services in the economy. Economic theory is primarily concerned with allocating these resources so that the production of goods and services is done most efficiently and effectively.

There are four general types of economic resources:

Land or natural resources

Labor

Capital

Entrepreneurial ability

Before we get into the specific categories of economic resources and how they are used to produce the entire economy’s goods and services, we’ll first discuss the idea of scarcity which is the problem of limited resources and unlimited wants.

The goal of economic systems is to satisfy the needs and wants of consumers. However, with scarce resources, we must choose how to allocate them to achieve optimal outcomes. Allocating scarce resources is one of the fundamental problems in both business and economics. One important tool for this is called the production possibilities frontier. It’s a tool for understanding the optimal outputs when producing different goods using the same resources.

From a macroeconomic perspective, scarcity happens since there’s a limited supply of natural resources in the world. For this reason, basic economic theory is concerned with allocating all the inputs of production to maximize prosperity and economic growth.

Similarly, microeconomic theory focuses on how individuals, households, or businesses make decisions using the resources they have. The limited supply of resources for individuals or companies is an outcome of their affordability. Meaning the number of productive resources an individual or firm owns is a consequence of how much they can afford to pay for them.

Microeconomic theory is thus concerned with how individuals make choices in using their resources optimally—i.e., what is the most cost-effective way of maximizing the utility of the resources owned.

Economic resources are the different factors of production used to produce all goods and services in the economy.

Land refers to all the natural resources used in the economy. In the most basic sense, land is required to produce anything. A business might use land to grow corn, dig for oil, build a factory, or mine cryptocurrency. Even in today’s modern economy, it’s hard to imagine producing anything without the right to the use of land.

This category of land also includes natural resources such as gold, silver, oil, or even wind, which is used to produce electricity. This is why some countries are considered rich in one economic resource but poor in another. For example, Australia is known for its vast iron ore, copper, and nickel. Saudi Arabia is rich in its enormous amounts of oil, and Brazil is rich in timber. These countries will trade land for other economic resources.

Labor refers to the different human resources involved in economic activity. The production of all goods and services necessitates the input of human labor. Human resources can vary from a waiter at a restaurant, a school teacher, an architect who designs the structure of a building, the artist who creates the interior of the building, and the workers who build it. Some businesses demand large amounts of labor, while others may need only a minimum amount. Further, all workers have different skills and capacities, so it is vital that each business correctly aligns the skill types needed for each task. For example, it would be a financial loss if a jewelry store assigned an expert in cutting diamonds to clean the store windows since the labor cost for cleaning windows is cheaper than the labor cost for cutting diamonds.

Capital refers to all physical assets that enable a business to operate. The term capital in economics refers to all means of investments used to produce and manufacture other goods. One main component of capital is financial capital—this includes money or other financial means like loans. But besides money, capital can be thought of as factories, machinery, technologies, patents, or licenses. These things are the capital that enables a business to operate.

Entrepreneurship is the capacity of an individual or a group of innovators who want to provide a particular good or service to the market. Entrepreneurship includes skills like innovating new forms of production, inventing new technologies, and organizing and managing a business. It entails the individual or group of people to invest their own capital in their business. This means an entrepreneur takes on a certain amount of risk when starting any type of business. The risk can be in the form of using one’s own money to get their business started; they spend their time and resources on an idea that they believe will eventually be able to create financial profits. Ideally, the entrepreneur’s risk-taking is rewarded by the financial profits made in the new idea or business. Thus entrepreneurship is an essential economic resource since no new firms or inventions will form without it.

Every business includes some degree of these four economic resources. However, depending on the industry and its position in it, each business will determine which economic resources it needs most and at what price it is willing to pay for it.

Many factors determine the price of and access to economic resources. The cost of all resources is an outcome of the degree of scarcity. Many factors cause scarcity; bad weather can make it harder to grow certain vegetables, or new immigration laws can cause a labor shortage. The nature and size of scarcity thus dictate all the choices made throughout the entire economy.

To see how the scarcity of resources impacts the economy, let’s take the example of a car manufacturer. First, they obviously need land to build a factory (capital). Second, they need money to buy raw materials, which is another type of capital. Third, they need labor which are the workers of the company. Finally, the business owners are the entrepreneurs.

However, depending on many factors, car manufacturing company owners will have to decide how to best use their economic resources. Should they spend money investing in a cutting-edge assembly line so that they will need fewer workers (labor) in the future? Or should they spend their money on buying raw materials today in case the price of those materials will drastically rise in the future?

Economists refer to these calculations as the “opportunity cost,” which means that by choosing one thing, you lose the potential gain of the alternative choice. Suppose the car company spends its financial capital on buying cheap materials today. In that case, it will not be able to invest in the development of new machines to automate its assembly line for tomorrow. The scarcity of economic resources forces business owners and managers to constantly decide how to best use them. If a business does not use its economic resources most efficiently, it will likely not succeed in the long run. This is because another firm will be able to produce the same product at a cheaper cost by correctly allocating its economic resources. So the success of any business, and the economy at large, requires using the four economic resources most optimally.

Outlier (from the co-founder of MasterClass) has brought together some of the world's best instructors, game designers, and filmmakers to create the future of online college.

Check out these related courses:

Economics

Here’s an overview of total surplus. Learn its definition, the different types of surplus, their uses, and how to calculate them

Subject Matter Expert

College Success

Great jobs for economics majors are out there! Learn the different opportunities available, what you can do with your degree, plus useful job search tips.

Subject Matter Expert

Economics

Learn about consumer and producer surplus, their formula, how they affect the economy, and how the elasticity of goods can affect them.

Subject Matter Expert